Photo by Wang Zhao/AFP/Getty Images

Singapore – Across Southeast Asia, there is a fierce battle raging for e-wallet dominance. E-wallets, or digital or mobile wallets, are types of payment instruments that can be used to transact at physical locations and online. These wallets can be linked to debit cards and credit cards or to a bank account and can also be loaded with a sum of money, called “stored value.” In some instances, e-wallets can also store cryptocurrencies.

Singapore – Across Southeast Asia, there is a fierce battle raging for e-wallet dominance. E-wallets, or digital or mobile wallets, are types of payment instruments that can be used to transact at physical locations and online. These wallets can be linked to debit cards and credit cards or to a bank account and can also be loaded with a sum of money, called “stored value.” In some instances, e-wallets can also store cryptocurrencies.

Riding the wave of rapidly increasing mobile Internet adoption by a 600 million person consumer base, telephone companies, banks, merchants, device manufacturers, transportation providers, remittance players, and consumer tech firms have recently set up e-wallets in Southeast Asia, aggressively competing for both consumer and merchant adoption.

Riding the wave of rapidly increasing mobile Internet adoption by a 600 million person consumer base, telephone companies, banks, merchants, device manufacturers, transportation providers, remittance players, and consumer tech firms have recently set up e-wallets in Southeast Asia, aggressively competing for both consumer and merchant adoption.

While payment volume through e-wallets is still a small proportion of noncash payments today, it is forecasted to scale rapidly. Mobile payments in the ASEAN region are expected to reach over $30 billion by 2021, of which e-wallets will capture a significant part.

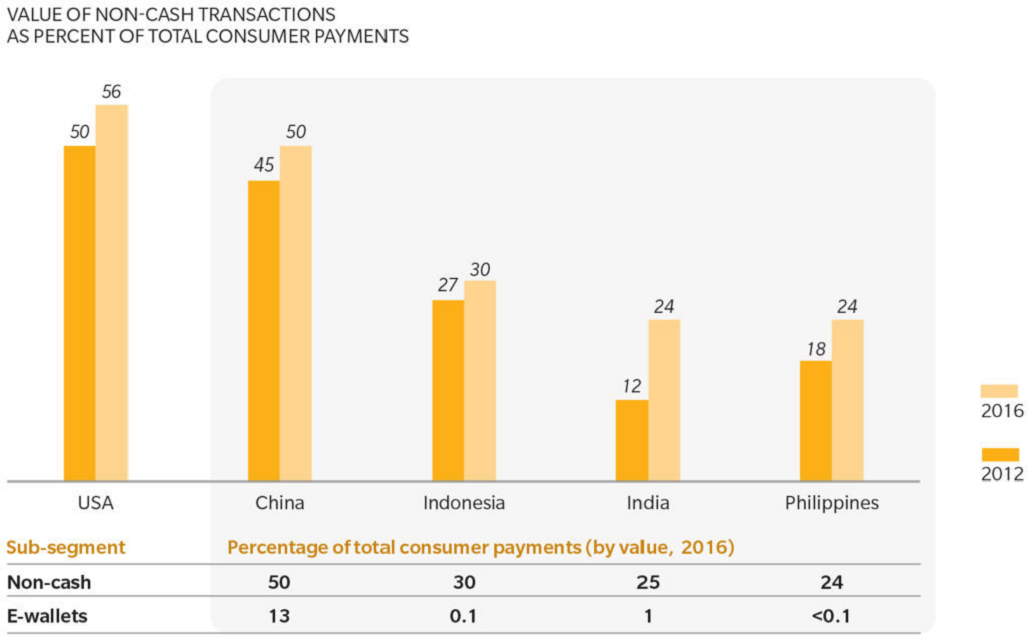

Exhibit 1: Share of Noncash Payments (of Consumer Payments) and Penetration of E-Wallet Payments within Noncash Payments (Source: International, eMarketer, Oxford Economics, Reserve Bank of India)

Although there has been a flurry of activity in the e-wallet domain, there are several challenges that must be considered for businesses to be successful.

Challenges Faced

Investors have actively supported these new businesses, but not all e-wallet companies will survive. Investors and e-wallet operators need robust business models that can sustain competitive differentiation and rapidly scale to stand a chance of success. In markets that are well past the tipping point of mass adoption of e-wallets, such as in Kenya and China, the evidence is clear—this is a winner-takes-all market, in which the top two players capture over 80 percent of the market. For any operator of an e-wallet, this should ring alarm bells.

As e-wallet adoption increases among the banked population, it also raises important strategic questions for the banks themselves, which have much to lose in both payment flows and consumer spend data. Payment flows may shift away from banks’ credit and debit cards onto stored value wallets, and even if cards are still the funding source for the wallets, then banks still lose visibility of payment behavior made from the e-wallet.

Markets in the region are at very different stages of evolution when it comes to e-wallets adoption, though different e-wallet business models are emerging. For instance, in China, e-wallet adoption grew beyond the tipping point early in this decade, driven by Alibaba and Tencent, setting the precedent for future evolution in Southeast Asia. Currently, the Philippines is on the cusp of a digital payment revolution, with noncash payment methods, particularly e-wallets, expected to surge to 6 percent of payments by 2022 from a tiny fraction today. This makes a pan-Southeast Asian e-wallet network difficult as integration in markets at different stages of adoption is a hurdle.

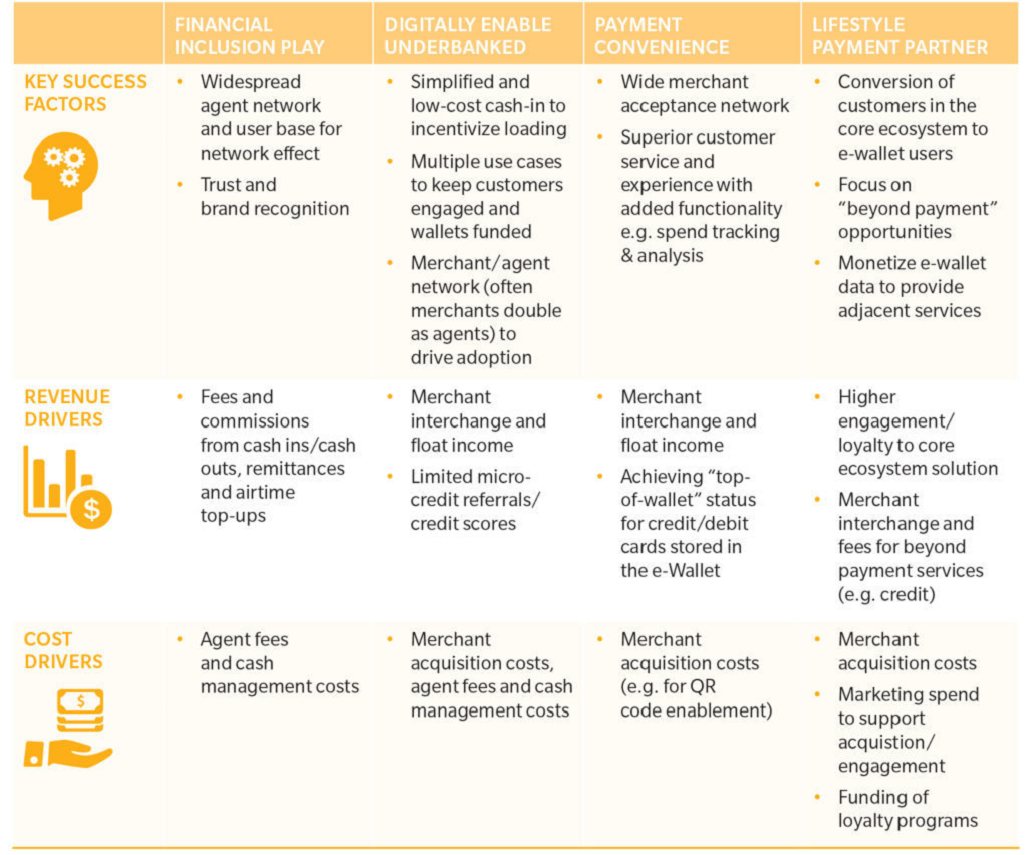

Different Winning E-Wallet Business Models

As e-wallets proliferate across the region, it is imperative to understand which players and business models will win the battle for supremacy.

Archetype A

The “Financial Inclusion” e-wallet, archetype A, targets the unbanked or underbanked, providing an e-wallet that is a digital alternative to holding physical cash. It is likely to be one of this demographic’s first experiences with formal financial services. For the unbanked, it is the closest substitute to a bank account, with primary uses being cash in and cash out, domestic and cross-border remittances, and limited payments—for example, prepaid mobile top ups.

Archetype B

Under “Digitally Enabling the Underbanked,” archetype B, leading players provide a wider range of quasi-banking solutions to the unbanked or underbanked segment. The e-wallet becomes a critical instrument to enable a broader set of payment use cases, and winners may need to provide value-added solutions that go beyond payments, such as providing simple advice on spending and budgeting and enabling credit solutions.

Archetype C

With “Payment Convenience,” archetype C, e-wallet operators target the banked segments, positioning their e-wallets as a convenient payment instrument to drive loyalty. Various models exist, but typically the e-wallet either stores credit and debit card data to enable those cards to be used in mobile payments, such as a device wallet like Apple Pay, or draws funds into a stored value facility, which is used to make mobile payments, for example, DBS’ PayLah. Revenue is driven by the interchange fees from the mobile payments made at merchants from the e-wallet and from finding ways to monetize the rich transaction data gathered each time the e-wallets are used.

Archetype D

Becoming the “Lifestyle Payment Partner,” archetype D, is the target end-state for many e-wallet providers, but few have achieved it, and even fewer bank-led e-wallets count among those who have. While banks might aspire to achieve this dominance, it is the large consumer tech platforms in frequent-use ecosystems, for instance, messaging platforms and e-commerce players, that are emerging as leaders. These players are merging e-wallet capabilities into their core offerings, encouraging captive users to adopt their e-wallet as an attractive payment alternative on its platform. The advantage of these ecosystem players is that monetization of the e-wallet does not have to come directly from payments, but instead from driving up the average ecosystem revenue per user.

Exhibit 2: Comparison of E-Wallet Archetypes

(Source: Oliver Wyman)

Time for Action

The tipping point for mass adoption of e-wallets across Southeast Asia is hard to predict, though trends in consumer behavior, technology advancement, and the evolution of ecosystem-based financial services all point to rapid acceleration in the next 3-5 years. Market infrastructure developments, such as real-time payments infrastructure, innovation in low-cost merchant acquiring, regulations on e-wallet onboarding requirements, and transaction value thresholds, will impact adoption and potentially change the fundamental shape of the retail payments landscape.

Investors and operators of e-wallets will need to manage the high costs of developing large networks to maintain their competitive edge, creating ubiquitous payments use cases, attracting users and motivating regular use. The path to monetization will be long and hard, but the rewards from becoming the indispensable payment instrument of choice for target segments will be huge.

Meanwhile, there is no room for complacency for banks and other existing payments players. With e-wallets emerging as the potential instrument of choice for small ticket payments, it is imperative that incumbents respond to defend their turf in retail payments. Banks need to make important strategic choices about where and how to compete, as they determine whether to participate directly with their own e-wallets or ensure how their own payment solutions are seamlessly integrated into the wallet platforms of future winners.

The full report can be accessed here.

Related themes: Disruption Investment Risk Mitigation

Duncan Woods

Duncan Woods

Partner and Head of Retail and Business Banking

APR at Oliver Wyman

Duncan Woods is a partner in the Retail & Business Banking practice of Oliver Wyman based in Singapore. Prior to joining Oliver Wyman, Duncan worked for Standard Chartered Bank where his roles included: Group Head of Strategy for Consumer Banking; Regional Head of Consumer Banking, Southern Africa; Regional Head of Priority Banking, Singapore and ASEAN; Group Head of Alliances, Consumer Banking. Duncan’s other experience is with Deutsche Bank and McKinsey. Duncan has a BA in Economics from Cambridge University, an MSc in Economics from University College London, and spent a year at Harvard Graduate School of Arts & Science on a Kennedy Scholarship.

The Battle for E-Wallet Supremacy in Southeast Asia

Asian Banks Need to Rethink Digital Banking

Banking the Unbanked in Southeast Asia: How can Digital Finance Help?

Nihal George

Nihal George

Principal, Digital, Technology and Analytics,

APR at Oliver Wyman

Nihal George is a principal in the digital, technology and analytics practice based in Singapore. He brings over a decade of experience spanning financial services, fintech startups, and management consulting. His work focuses on designing and implementing new business models, digital transformation and organizational change.

The Battle for E-Wallet Supremacy in Southeast Asia

Anosh Pardiwalla

Anosh Pardiwalla

Associate, Financial Services at Oliver Wyman

Anosh Pardiwalla is a strategy & operations consultant with global experience stretching across large scale implementation projects for marquee clients. Prior to his move into the consulting field, he developed new business opportunities for his previous company across the Oil & Gas, Steel and Petrochemicals sectors. He currently focuses on digital payments and associated payment opportunities in the digital and e-commerce space.

The Battle for E-Wallet Supremacy in Southeast Asia

The article can be read at Brink Asia website.

Leave a Reply