As another year draws to a close, East & Partners look forward at what business banking has in store and the market in the years ahead.

Supply Chain Financing Reaches A Tipping Point

Supply chain financing (SCF) now, especially in Asia, is characterized by a relatively low adoption rate, mired with multiple interpretations of what the terms actually mean, and a lack of understanding of the products and their benefits among businesses. Compared with other types of trade financing, SCF has a somewhat “stickier” relationship and tends to follow the overall corporate banking relationship.

Supply chain financing (SCF) now, especially in Asia, is characterized by a relatively low adoption rate, mired with multiple interpretations of what the terms actually mean, and a lack of understanding of the products and their benefits among businesses. Compared with other types of trade financing, SCF has a somewhat “stickier” relationship and tends to follow the overall corporate banking relationship.

The tide is turning, however. With digitisation enabling efficient data sharing across stakeholders, improving traceability and visibility of the entire supply chain, it is easier for all players in the ecosystem to leverage it. Combined with an increased awareness and understanding of the various solutions, we see growing demand for SCF. In fact, recent East & Partners research suggests winning SCF businesses could potentially open doors for new banking relationships.

Evolving Demand for Cross-Border Payments and FX

Against the more challenging macro environment driven by increasing US-China trade tensions, rising risk of global recession, as well as uncertainties surrounding Brexit and civil unrest in some markets, businesses are prioritising FX risk management above other trade financing initiatives.

While poor visibility of payment status and a lack of payment timing predictability remain major cross-border payments pain points for businesses, compliance requirements are becoming increasingly difficult. This is aggravated by the fact that most corporates maintain local bank accounts in the markets they make cross-border payments to, where they are also facing challenges when opening and operating these accounts. Is your bank ready to cater to these evolving corporate needs?

Value for Money: Secret to Winning Corporate Customers’ Hearts

Value for Money has been consistently highlighted as a core service metric for businesses deciding on their transaction banking provider, and it is a trend likely to stick. Close to one in four (23.7 percent) large corporates in Asia have nominated Value for Money as the most important attribute in their bank relationships, ahead of Understanding of Customer’s Business (19.7 percent), Credit Approval Turnaround Times (16.6 percent), Effectiveness of Problem Resolution (8.9 percent), Quality of Customer Support (8.2 percent) and Quality of Overall Service Delivery (7.2 percent).

Interestingly, when asked about the main reasons for corporates to switch provider, Value for Money is also cited as the leading driver of attrition. This further reinforces the importance of banks seeking ways to add value to their customer relationships if they wish to stay ahead of the game.

Curiously, though, banks are not paying enough attention to this critical service factor. Businesses’ dissatisfaction with Value for Money is rising across the market in general, be it with their trade financiers or their transaction banks.

Value for Money is undoubtedly a fluid concept. Depending on the industry sector and business size, it may be seen as having the lowest cost, offering exceptional service, advising on best trading strategies to follow, giving guidance on emerging market opportunities, offering integration with other products, making introductions to other relevant clients, or a combination of some of these.

The trick lies in choosing the right focus for each target segment. While small and medium-sized enterprises (SME) tend to associate Value for Money with competitive pricing, large corporates and institutions are enticed by exceptional service, benchmark insights and “something special”.

Fintech Hype Falling Short for CFOs

While blockchain is positioned as a solution to every problem for banks, practical real-world solutions are fleeting. ‘Blockchain fatigue’ is replacing the hype that followed the proliferation of distributed ledger technology (DLT) developments launched by banks and various consortia in the last five years.

As the buzzwords lose their fizz, when will corporates finally see the much-vaunted benefits?

Wide scale adoption beyond traditional applications remains limited, for example projects applying blockchain to ID fraudulent goods down a supply chains have faded into obscurity with barely a whimper. Successful supply chain blockchain launches are yet to eventuate in earnest, evidenced by IBM settling for blockchain simply forming a component of more complex systems in a ‘shadow ledger’ style unable to stand on its own two feet…yet.

Effective financial technology delivery hinges on truly understanding the voice of the customer – not producing another ‘solution looking for a problem’. Time is running out for banks to deliver.

FX Risk Management Becoming Critical for all Businesses

With financial markets tested with economic, environmental and political volatility, it has never been more imperative for corporates managing large scale international operations to implement a coherent, proven currency risk management strategy to minimise downside risks associated with currency fluctuations.

There has been a growing trend in the use of risk management products such as FX Options and Forward FX as strategic approaches to mitigating risks. Businesses with revenues of US$20 million and greater tend to a higher level of derivatives hedging usage due to a higher level of trade and supply chain dispersion.

It is important to note however that there has been significant growth in the use of risk management products among SMEs in recent rounds of our research. These trends are set to continue as global FX markets brace for increased uncertainty in the wake of Brexit deliberations and unpredictable US-China Trade war negotiations.

Digitisation Pipe Dream Becoming a Reality

Trade finance continues to be a paper dominated process, with estimates suggesting up to three quarters of all transactions are processed manually. Despite automation, artificial intelligence and machine learning streamlining credit approval and compliance decision making, trade remains frustratingly burdened with costly and error prone approval.

While major trade finance providers such as HSBC, Citigroup, Standard Chartered and ANZ announce new collaborations designed to lurch trade finance into the 21st century, digital transformation remains nascent.

Long overdue advances in trade finance automation and straight-through-processing (STP) such as digital platforms, smart contracts and the Internet of Things (IoT) could radically reduce administrative costs, transaction fees and clunky document heavy processing delays.

Less friction undoubtedly will result in greater cross border goods and services flows in an area which has been criticised for falling behind the pace of digital innovation taking place in other business banking product lines such as transaction banking and payments. Trade transactions are still commonly assessed over several weeks instead of same day or instant.

Benefits of digitisation include faster transaction speed, lower costs, improved customer wallet share, more appropriate facility matching, less administrative error correction and reduced fraud risk.

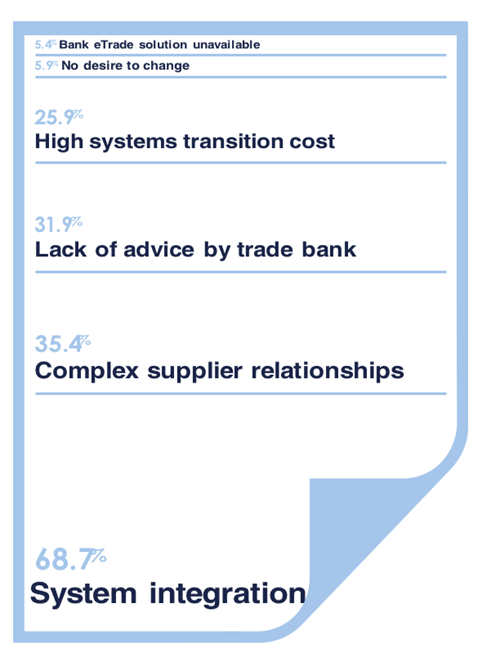

Difficulties in linking disparate stakeholders including corporates, carriers and banks results in issues applying standardisation to electronic bills of lading (e-bills) not to mention complex legal implications. Streamlining these processes is a much-needed step in the right direction and a clear impediment to change is industry collaboration, requiring an ‘all or nothing’ approach to digitisation.

Customer expectations are quickly running ahead of what banks can reliably offer, evidenced by declining value for money perceptions across all segments, sectors, regions and trade profiles.

Can banks’ trade product and service offerings keep pace with customer expectations? Providing practical guidance on innovation, allocating a knowledgeable trade account officer and limiting rising customer churn will be the telling factors for success in trade in 2020 and beyond.

Fintech Hype Falling Short for CFOs

% of Total

Can Banks Afford to Become the Advisors CFOs Need…Or Can They Afford Not To?

Banks may acknowledge the threat nimble new entrants and Fintech disrupters pose to their business model yet do they truly understand what is driving increased customer churn? What factor is driving the changing behavioural trends?

As the low interest rate environment pressures bank profitability, the solution to sliding wallet share resides in meaningful customer engagement – not less. Automation may save costs but at what expense? East & Partners research reveals incumbent banking majors are struggling to keep up with a customer base eager to explore new opportunities.

Customer switching intentions have surpassed record highs last seen before the 2008 Global Financial Crisis. Even ‘home banked’ small businesses traditionally unwilling to multibank for their transaction banking or lending needs are sitting up and taking notice of new offerings.

With businesses more likely to turn to friends and colleagues than their relationship manager for complex advice tomorrows leading banks will be those that recalibrate business banking relationships to that of proactivity.

Competition Contributes to Customer Care

Business FX markets are experiencing a dramatic increase in competition as a broad array of ambitious new entrant’s scramble for growth opportunities. As a result, the market has become extremely fragmented, evidenced by declining average wallet share in our long running Business FX research. This trend has driven incumbent providers to step up and deliver better quality service to their clients lest they end up suffering damaging customer churn.

The number of providers importers and exporters regularly use for Spot FX transactions continues to expand in line with rising churn intentions. This has not only been evident in Spot FX but also risk management products, particularly for larger sized middle market corporates. In order to remain competitive, major FX providers have been forced into a position to improve and develop their services to corporate customers.

Non-Banks Begin to Win the Minds of Corporates

As banks fail to differentiate themselves and continue depending on outdated marketing strategies, legacy systems and passive customer referrals, non-banks are leveraging market share opportunities by labelling themselves as ‘innovative Fintechs’. This approach has been gradually capturing ‘mind share’ with corporates eager to align with a fresh ‘look and feel’ to their business banking services.

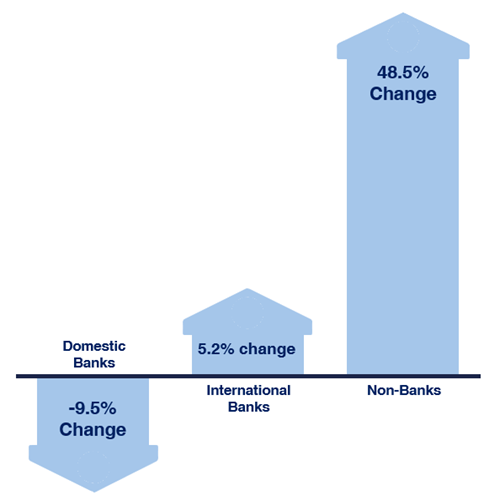

Since H1 2018, unprompted brand recall (mind share) has been steadily increasing for non-banks in aggregate across several markets, while international banks stagnate and domestic banks decline. Mind share is a vital leading indicator of new relationship share growth particularly among CFOs and corporate treasurers expressing rising dissatisfaction with high street banks. Micro businesses and SMEs tend to be more susceptible to the noise in the market in the hope of discovering a better alternative.

At present, banks still remain as mind share leaders across all business sizes however the growing trends that have emerged in the market pose a considerable threat. Although increased mind share does not directly translate into increased market share, if the current market mind shares trends continue, then in the next five to ten years non-banks will have certainly won hard fought market share away from major global banks as well as regional and national banks.

Part of the impetus behind this trend is strong customer advocacy. Active customer advocates of any business banking brand will undoubtedly boost brand awareness in an industry saturated with competition. Due to the increasing number of new entrants competing with banks even for core transaction banking and lending services, it is extremely difficult to stand out. Non-banks are gradually getting their proposition right among business customers.

Non-banks return excellent customer advocacy ratings compared to domestic and international banks, with a greater number of active brand advocates willing to promote their brand positively. This trend has been more evident with secondary customers compared to primary customers. In the long run can non-banks harness improving mind share and customer advocacy ratings as the incumbent big bank majors fight back?

Non-Banks Begin to Win the Minds of Corporates

To subscribe to East & Partners newsletter, click HERE.

Leave a Reply