By Alex Rolf

No trend is more reliable than transaction banking (TB) retaining its much-vaunted position as the bedrock of commercial banking customer engagement and relationship management strength.

Across cash management, payment processing and cross border payments, corporates start and finish their assessment of a Bank’s overall competence predicated on overall TB capability.

As CFOs and corporate treasurers shift from COVID-19 pandemic “shell shock” in 2020, acceptance in 2021 and now adaption in 2022, where should incumbent TB leaders invest to retain clients growing increasingly impatient with the level of new functionality available to them?

Conversely how must challenger TBs successfully scale up for growth?

Technology Transformation

The accelerated rate of digitalisation following the pandemic has forced corporates towards a markedly different product and service proposition. Treasury services are overlapping with information technology (IT) and CTO responsibilities more frequently.

East & Partners research suggests treasury professionals are struggling to deliver on the rapid rate of innovation in the core TB function, placing severe pressure on key decision makers to meet rising internal liquidity and cash forecasting benchmarks on a wider scale.

“Corporates have never been more motivated to implement treasury services automation, reflected in record high switching intentions. If their primary transaction bank cannot meet their rising expectations, they are ready and willing to switch”

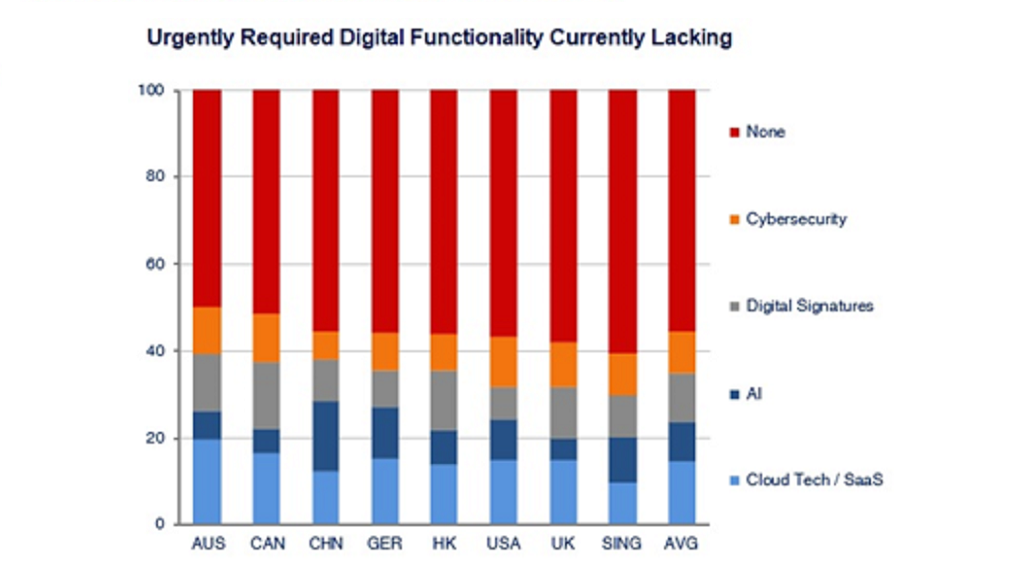

East & Partners 2021 Global Insight Report “Bank Relationship Management Post COVID” confirms a high proportion of large corporates are crying out for digital functionality they do not currently have access to yet urgently require (44 percent).

14 percent of large corporates need cloud technology and software-as-a-service (SaaS) support. One in ten are seeking e-Documentation support, particularly in trade finance (11 percent), require greater support for fraud protection (10 percent) or want to learn more about artificial intelligence (9 percent).

In 2020, within the enterprise application software market, the cloud market became larger than the non-cloud market for the first time primarily driven by COVID.

Electronic Service Delivery satisfaction ratings jumped three points year-on-year in the Australian middle market from 1.44 to 1.41 on a one to five scale where 1 = satisfied to 5 = dissatisfied, indicating the largest single year improvement in the last decade.

The Big Four majors in Australia and key international TBs including HSBC and Citigroup are clearly fighting back against acquisitive domestic and international rivals such as BoQ, Suncorp and JPMorgan.

The main focus however falls on the aggregate “Other” total of TBs outside the top eleven nominated providers. This figure has more than doubled since 2019 from 0.6 percent to 1.2 percent, albeit from a low base, indicating competition is intensifying beyond the traditional playing field.

Post-Crisis Customer Churn Leaping Forward

Middle market enterprises are becoming increasingly less likely to bank in a holistic way, opting instead to ‘shop around’ for competitive pricing and improved service in lock step with their larger corporate counterparts as opposed to SMEs allocating the majority of their TB wallet to their primary provider.

“Really getting on top of fully digitising our cash and payments. Our home bank is actually ahead of the curve and we are maybe 70 percent of the way there.” Group Treasurer, US$10Bn Singaporean Wholesale Distributor

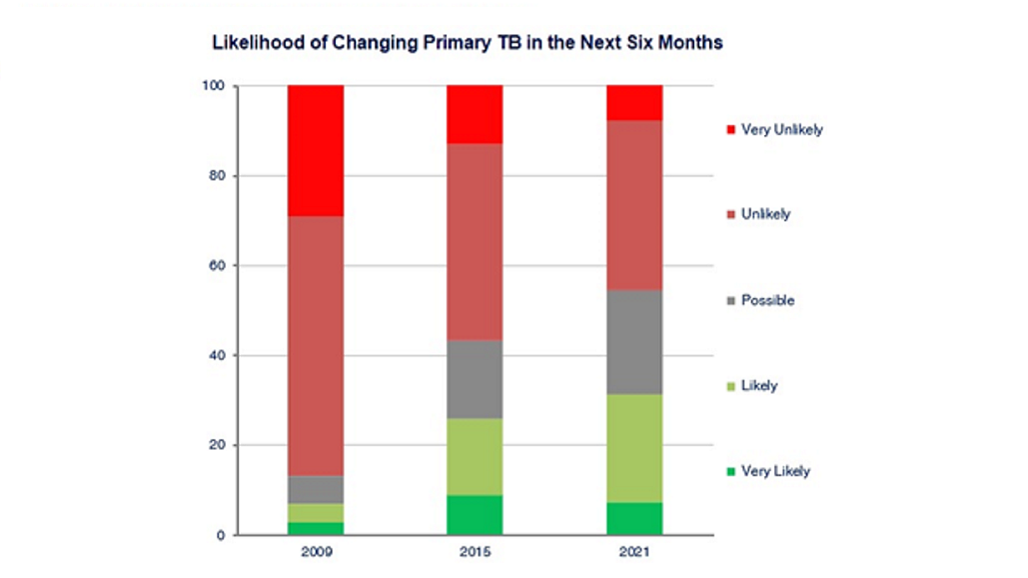

Customer churn intentions have reached record highs, exceeding the pre-Global Financial Crisis (GFC) peak by a significant margin with one in three corporates likely to change TB in the next six months (31 percent).

Currently just under one in two corporates are unlikely to switch (46 percent) yet during the GFC as many as nine out of ten corporates were unlikely to switch (87 percent).

“In Asia, we are seeing a rise in demand for co-creation in this flight to digital TB. A majority of the corporates in the region view co-developing or simply buying business specific digital solutions from their banks as a way forward.” East & Partners Asia Business Head, Sangiita Yoon.

As technology and TB become more closely intertwined, are traditional powerhouse TBs still fitting into the equation for CFOs? For many leading TBs the solution has been to partner with FinTechs or acquire them outright to ensure they keep pace with competition.

As the race heats up for TB dominance, challenger TBs are well placed to win relationship share away from ingrained market leaders who have enjoyed “sticky” customers for the better part of ten years. Specific digital functionality is the difference between merely becoming a secondary TB on the fringes or fully supplanting primary TBs with the onus firmly placed on value for money in 2022 and beyond.

Original article can be viewed HERE.

Leave a Reply