The ABA Policy Advocacy Committee held on October 27, 2022 its third meeting of 2022 featuring two relevant position papers on Data Analytics and the Hybrid Work Environment emerging out of the pandemics.

The online meeting started with Mr. Eugene S. Acevedo, ABA Chairman and President and CEO of Rizal Commercial Banking Corporation (RCBC) from the Philippines, welcoming the 246 registered participants.

Ms. Christina M. Alvarez, current Chairman of the ABA Policy Advocacy Committee and Senior Vice President and Head of Corporate Planning Group at RCBC, also welcomed the participants and thanked the two paper presenters for their valuable contribution to the policy advocacy work of the Association.

I. SUMMARY

(1) The first paper on “Application of Data Analytics” presented by Mr. Kenny Au, Head of Data Science & Governance Department, Technology and Productivity Division at The Bank of East Asia, Limited, explained the Bank’s experience and practices in the use of data analytics to achieve effective decision-making in the organization. The paper elaborated on how BEA applies data analytics to gain better customer insight, improved operations, more insightful market intelligence, agile supply chain management, data-driven innovation, and smarter recommendations and targeting, among others.

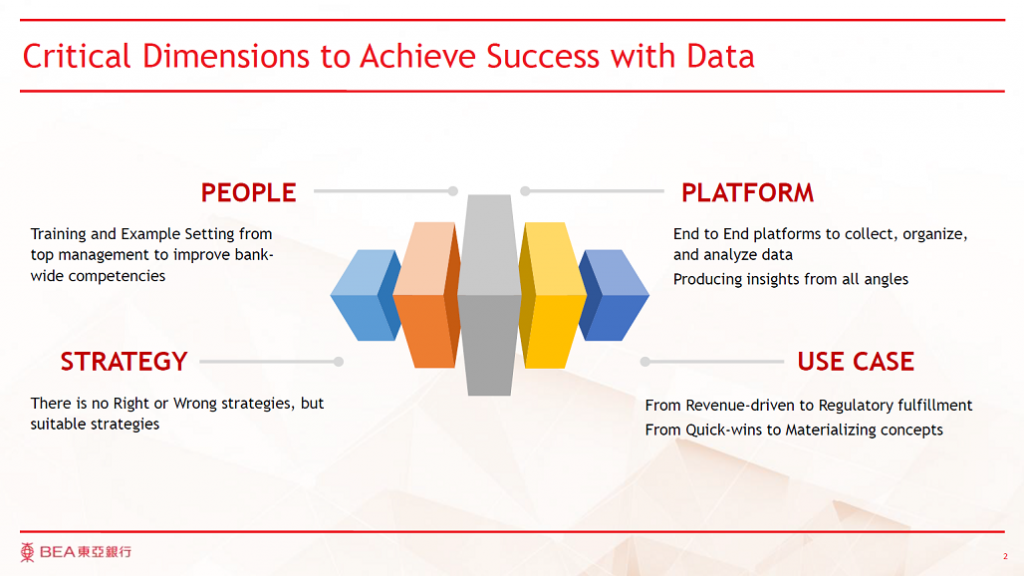

Mr. Au noted that with the rising awareness of the importance of data, organizations have begun to incorporate data analytics into their digital transformation journey. In the position paper, he pointed out that from data preparation, governance, to visual analytics, there are numerous theories and approaches used to achieve results. The paper discussed a structured approach, based on the People, Platform, Strategy, and Use Case, to show case a practical guide in applying data to an organization.

Following are the salient points raised by Mr. Au in the position paper:

PEOPLE — Data Literacy Empowerment

A series of industry recognizable training should prepare an organization for the necessary changes to become truly data driven. From top management to general staff, each hierarchy layers will be equipped with relevant levels of Data Literacy.

Data Leader (DL), including Board members, General Managers, and Head of Departments are expected to drive data culture, and support staff at all levels on both implementation and knowledge. Data Leaders will be setting visions and providing required resources for initiatives to come.

Citizen Data Scientists (CDS), usually nominate and selected by the Data Leaders, to promote data driven culture through enhancing technical capability over time.

Data Citizen (DC), open to bank-wide staff. Raising overall awareness as well as improved knowledge to think, speak, and act with data.

An ongoing Data Community will be created to ensure the productivity of use case generation, knowledge transfer and support of data usage.

External collaboration is encouraged to facilitate the training with required tools such as Data Visualization software.

PLATFORM — from Zero to Data Commercialization

In order to facilitate changes, specific foundations need to be constructed in parallel.

Storage: Traditional companies especially with a sizable operation often built their database gradually on a need basis approach. Databases are often designed and rolled out independently (silo), with a specific purpose, installed locally by different vendors. Naturally, a new storage infrastructure is required to match the need for safe, easy, structured, and stable access across the whole organization. Going Cloud is one inevitable option. Migrating existing data warehouse to cloud, prioritizing from front to back office will achieve just that.

Preparation: Although each data user is expected to prepare their own data. Nonetheless, group wide standards on Data Governance is a must. Setting up committees such as Data Council, to define rules and policies to uphold communication efficiency, data quality, and gate keeping security.

Process: Riding on good quality data source, AI and Machine Learning can take place. Users will be able to leverage Tagging Library, Visual Analytics to generate directions and insights which, in turn, helps decision makings.

STRATEGY — Data Adoption by Every Staff

A true data driven company requires every staff to engage in data. Roles and Responsibilities can first be separate Centralized Team from the rest of the non-data staff.

Centralized Team – Advanced analytics, modelling, and machine learning capabilities are expected to be developed by a centralized team led by the Data Team. They will act as a point of contact for the whole organization to provide guidance and support on both knowledge and practical initiatives.

Rest of Staff – A range of tools should be available for both senior and junior staff to access. For example, senior staff who needs to make management decisions on a daily basis can make use of Self-Service Market Place to be more informed and efficient.

USE CASE — Real-time Analysis

To ensure the practicality of the data journey, it is advised to go for a Use Case approach.

To gain trust and support from senior management, it is important to produce use cases that can bring in quick wins and return. Real-time analysis can be a useful option.

Example for banks:

- Significant account movement such as receiving a lump sum of cash

- Real-time analysis has performed to identify whether the cash deposit is:

- Fraud è which will be alerting relevant systems

- Legitimate transaction è provide simple recommendations such as investment advice if the cash came from selling a stock

In conclusion, Mr. Au pointed out the following on the foreseeable future of the data economy in banking:

Data will become more and more like a currency which can be used to monetize for both customers and banks, once the market has successfully tackled the “consent problem”.

Open Banking, where banks are sharing customer data (with consent) to third party service providers. They will be able to create products and services that can leverage looking at the whole picture of customers’ portfolios.

Open Finance, where banks are taking in alternative/external data (with consent) from third parties. This allows banks to create tailored financial products and services to individual customers with low costs.

He said that with the right preparation mentioned in previous sections, organizations should be able to take hold of the opportunities where data collection, preparation, analyze, and usage capability are fully ready.

(2) The second paper on “Hybrid Work Environment” by Ms. Nguyen Tuyet Duong, Member of Board of Directors of The Vietnam Bank for Agriculture and Rural Development (Agribank) explained their experience and practices in adopting to the new hybrid work environment in response to the COVID-19 pandemic.

Ms. Nguyen Tuyet Duong elaborated on measures the Bank took at the height of the pandemic to ensure employees had all the resources they needed to maintain their productivity while still hitting organizational goals. She also cited some of the changes emerging since employees have been returning to office as the pandemic eases, and what steps the Bank has taken to make the shift to a hybrid workplace and deal with the transition while maintaining productivity and increasing engagement levels without stressing the employees.

Ms. Duong reported that Agribank’s business activities have been affected by the pandemic more than other commercial banks in Vietnam mainly for two reasons: (a) its relatively large size and network, and (b) its particular customer base that is mainly consists of people living in agricultural and rural areas as well as the disadvantaged and vulnerable groups in society.

Ms. Duong pointed out that following the direction of the Government and the State Bank of Vietnam, Agribank has directed a drastic, flexible, and synchronized implementation of multiple policies as well as human and technological solutions to help mitigate the impact of the pandemic, continue to help support the economic growth of the country, while at the same time reach Agribank’s business target in 2021.

In order to achieve these objectives, Agribank has persistently and drastically implemented two-pronged solutions, namely: (a) quickly implement policies for staff members, for customers, and for the society; and (b) thoroughly benefit from the technological advantages and digital platforms alongside information security in all activities. Fortunately, Ms. Duong reported that in 2021, all nine business indicators of Agribank recorded growth. Agribank’s total means of payment grew by 8.93%, credit increased by 12.9%, and total assets went up by 8.3% compared with te levels in 2020.

Looking ahead, Ms. Duong said that Agribank has implemented strategic changes to adapt to and continue to develop the new normal. She said that Agribank’s Board of Directors has realized that in addition to short-term measures, long-terms solutions need to focus on organizational and personnel changes and that promoting digital transformation is an inevitable trend to help organizations to quickly adapt to the new normal after Covid-9 in order to grow faster and more sustainably.

In the short-term, Agribank will continue to bring the workforce back to the workplace, encourage and help increase productivity while raising awareness on pandemic prevention and control.

In the long-term, Agribank will focus on digital transformation based on modern technology with the aim of further improving competitiveness and customer experience to help Agribank overcome all difficulties and challenges.

In addition, Agribank plans to implement measures to help implement the national financial inclusion strategy in 2025 with a vision to 2030. These measures include:

Completing the legislation framework to create an enabling environment for achieving financial inclusion goals and conducting research work to identify and effectively manage risks related to financial inclusion;

Develop a variety of supply organizations, distribution channels, improve financial infrastructure, in order to support customers to access and use basic financial products and services conveniently at reasonable costs, and

Develop a variety of basic financial products and services, aiming towards the target of financial inclusion.

Because of the strategy it has adopted to mitigate the adverse impact of the pandemic, Agribank come to be known as a banking and financial institution that has done very well in the prevention and recovery of business activities. The Asian Banker has ranked 138 in the top 500 banks in the Asia Pacific region, recorded also as the highest level among commercial banks in Vietnam.

After the presentations, the Committee agreed to hold its next meeting in conjunction with the ABA Planning Committee Meeting to be held early 2023, the exact date and venue of which to be decided later.

II. PRESENTATION FILES

The presentation (PDF format) of the session can be downloaded HERE.

III. VIDEO

The video recording of the webinar can be viewed in the ABA YouTube:

Leave a Reply